Mon Nov 17 01:30:00 UTC 2025: Okay, here’s a news article summarizing the provided text:

Tata Motors Demerger: Commercial Vehicle Arm Makes Strong Market Debut, Tax Implications Explained

Mumbai, India – Shares of Tata Motors Commercial Vehicles (CV) business made a successful debut on the National Stock Exchange (NSE) on November 12, listing at ₹335 per share, a significant 28.5% premium over the discovered price. This listing marks the completion of Tata Motors’ demerger, separating its Passenger Vehicle (PV) and Commercial Vehicle (CV) businesses into two distinct, publicly traded entities.

The demerger has sparked investor interest not only in the strategic implications but also in the tax consequences for shareholders. When a company splits and shareholders receive shares in the new entity, questions arise about how to calculate the cost basis for tax purposes.

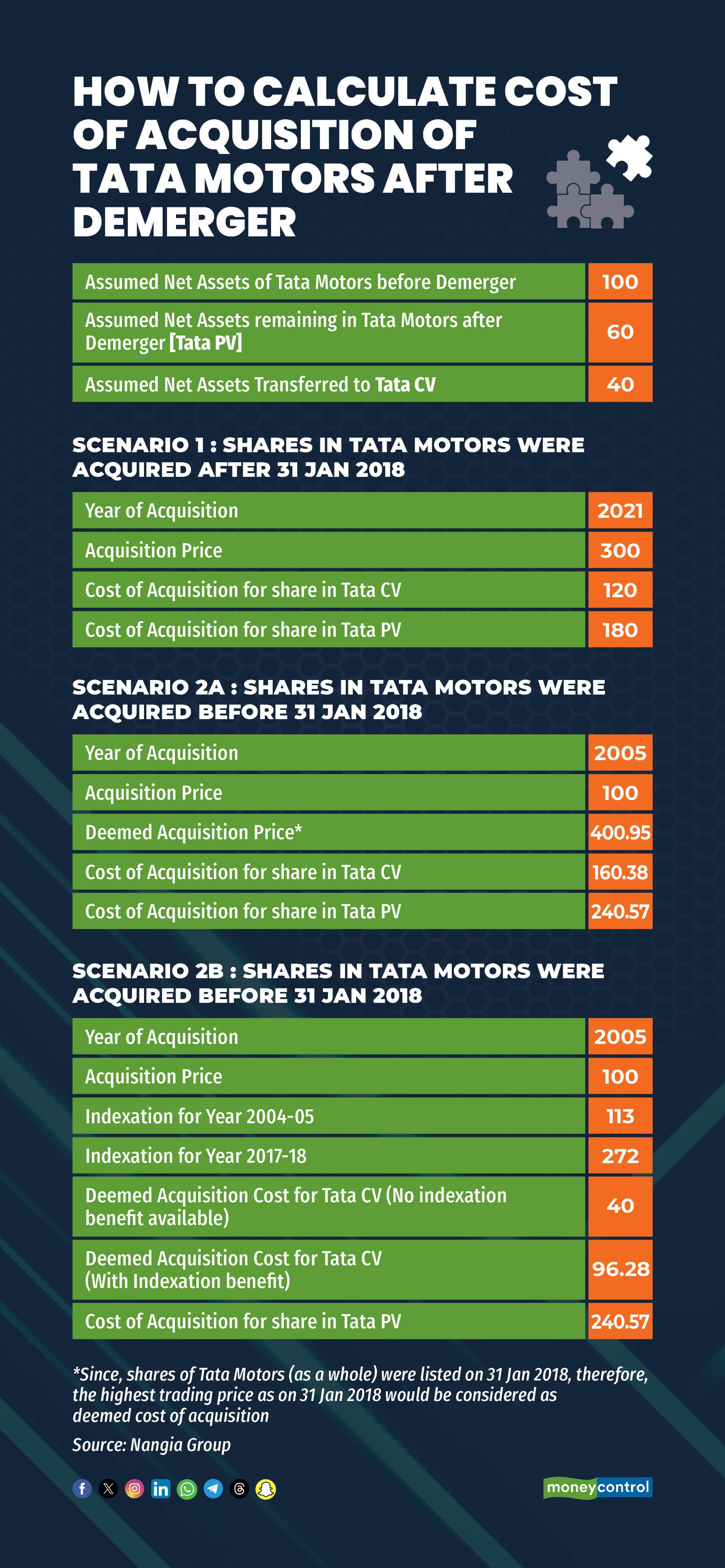

Abheet Sachdeva, Partner at Nangia Group, explained that under the Income-Tax Act, the original cost of acquiring shares in Tata Motors needs to be apportioned between the PV and CV businesses. The apportionment is based on the ratio of the net book value of assets transferred to the CV business to the net worth of Tata Motors as a whole before the demerger.

“For instance, if 40% of Tata Motors’ net assets were transferred to the CV business, then 40% of your original cost of Tata Motors shares becomes the cost of acquisition for your CV shares, while the remaining 60% applies to the PV shares,” Sachdeva noted.

The article further clarifies the “grandfathering” rule introduced in 2018, which allows investors holding listed shares as of January 31, 2018, to use the fair market value (FMV) on that date as the cost of acquisition. However, the direct application of the FMV benefit for the new CV shares may not be possible. Instead, the proportionate cost based on cost indexation could be used.

Sachdeva elaborated that while the FMV benefit might not be directly applicable to the CV shares, there’s an alternative approach using the grandfathering provisions, where FMV testing is done on the existing shares of the old company and the proportionate cost of those shares is considered the cost of acquisition of shares in new company.

Why This Matters

This information is crucial for investors when they eventually sell their PV or CV shares, as capital gains will be calculated using the apportioned cost of acquisition. The demerger itself is tax-neutral, meaning no tax is paid when the CV shares are initially allotted. The holding period for the new shares continues from the original purchase date of Tata Motors shares. Investors who held Tata Motors shares before the cut-off date may be eligible for FMV under the grandfathering rules for the PV side.

Additional Resources

For the latest business news, market updates, and personal finance insights, investors are encouraged to visit [Moneycontrol.com].